Range Safety & Air Filtration Systems Industry Analysis

Investment Thesis

The U.S. range safety & air-filtration sector is a $3–5B compliance-driven market anchored in the ~6,000 commercial and law-enforcement indoor ranges nationwide. The industry is highly fragmented, with hundreds of small HVAC contractors, environmental engineers, and niche range specialists controlling local markets but no scaled national provider. Core offerings include specialized HVAC/HEPA systems, filter replacements, compliance testing, and OSHA/EPA audits creating sticky, recurring revenue streams that resemble steady cash flow.

Growth is supported by 8–10% projected CAGR, driven by enforcement of rules around airborne lead exposure alongside modernization of law enforcement and military training ranges backed by state and federal budgets. Rising recreational shooting participation and consumer health awareness pose as main growth drivers giving rise to attractive investment dynamics in terms of low acquisition multiples and strong opportunity to bundle adjacent compliance services.

Overall, the sector presents a defensible, recurring-revenue niche with resilient demand, clear compliance tailwinds, and significant white space for a scaled consolidator to capture share and expand margins.

Industry Overview

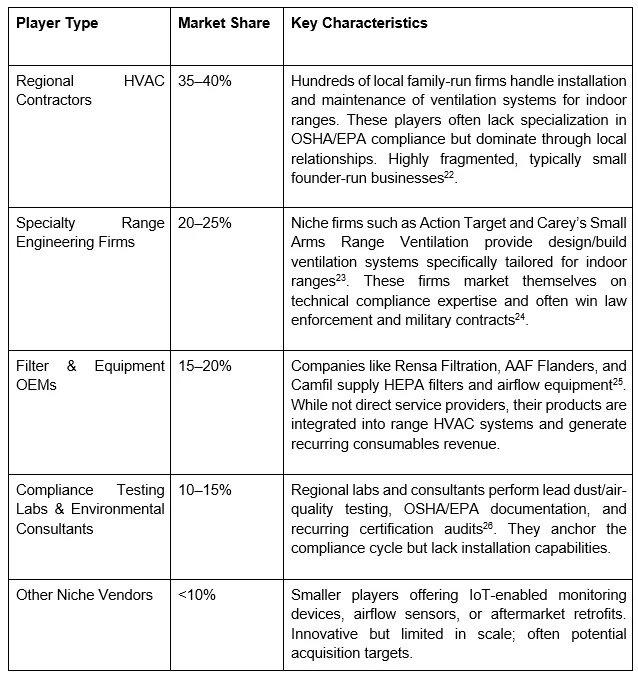

The U.S. Range Safety & Air Filtration industry is a fragmented environmental control and compliance sector serving approximately 6,000 commercial and law-enforcement indoor shooting ranges nationwide[1]. Core offerings include specialized HVAC and HEPA air-exchange systems, negative-pressure room designs, high-efficiency filters, and periodic OSHA/EPA-compliant testing. These systems typically include dedicated supply and exhaust air systems, negative-pressure configurations, laminar airflow, and HEPA-level filtration to protect both shooters and range personnel from elevated lead exposure risks[2].

As of 2025, the global indoor shooting range ventilation market size has reached $814.7M indicating the ever growing emphasis on safety and regulatory compliance in indoor firearms facilities. It is characterized and dominated by local HVAC integrators and specialized firms with limited geographic scope and no dominant national player. Many operators are small, founder-run firms with limited geographic reach, creating opportunities for consolidation. The market is experiencing vigorous expansion with a projected CAGR of 6.2% from 2025 to 2033[3]. This growth primarily stems from stricter enforcement of OSHA and EPA standards on airborne lead exposure, increasing investments in law enforcement and military infrastructure especially with the growing geopolitical tensions in the United States, alongside rising participation in recreational shooting sports[4] and heightened awareness of indoor air quality standards.

Overall, the industry is compliance driven, with recurring revenue anchored in consumables: filters, testing contracts and certification audits every few months[5]. This creates a perfect incubator for a recurring-revenue niche with resilience to economic cycles and strong parallels to other regulated environmental services industries.

Market Size & Growth

Total Addressable Market - $3-5B (U.S only)

The U.S market for indoor range ventilation and air-filtration systems is estimated at $3–5B annually. This figure was built from the bottom up with an approximate of 6,000 commercial and law-enforcement indoor shooting ranges nationwide, with an average per shooting range spend ranging anywhere from $500K- $833K. This figure includes initial HVAC/HEPA installations, retrofit projects & compliance services. Key drivers that underpin the Total Addressable Market are regulatory requirements in terms of OSHA and EPA standards, HEPA exhaust, lead exposure lawsuits and public health studies[6] and modernization of facilities by commercial operators and agencies.

Serviceable Available Market - $2.1B

The serviceable Available Market (SAM) addresses the portion of the TAM made up of shooting ranges...