The Goldman Bet: Why Full-Service Banks Are Buying VCs

Read the original at capraecapitalpartners.substack.com ↗

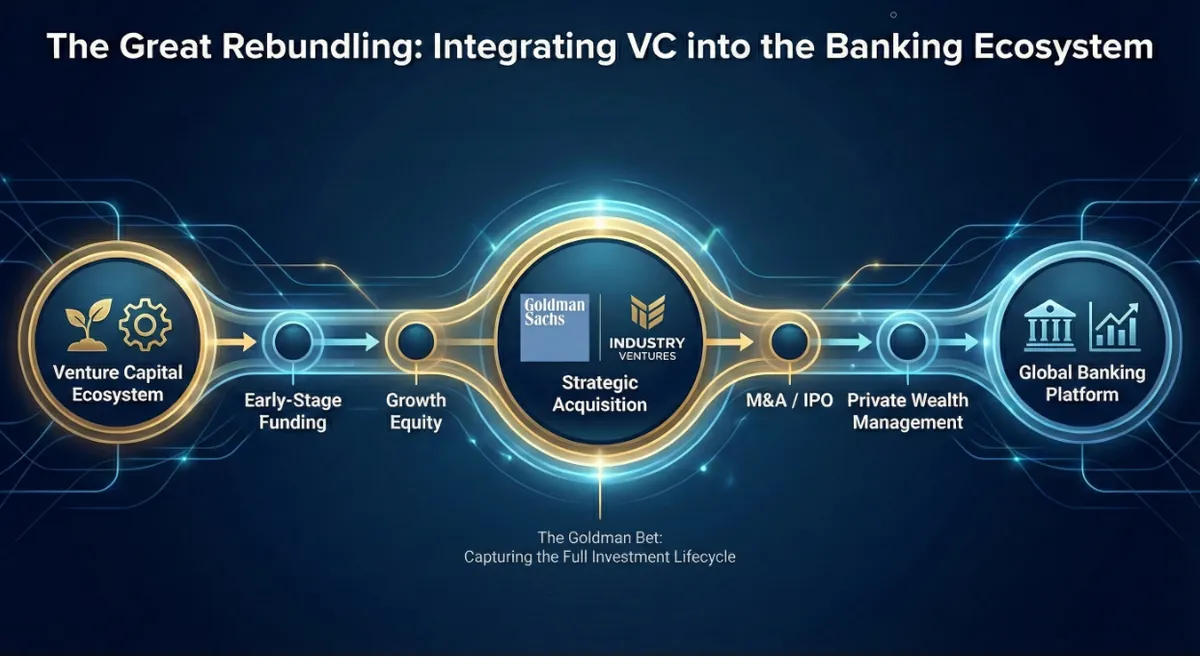

The acquisition of Industry Ventures by Goldman Sachs is not merely an asset-gathering exercise; it is the purchase of a time machine. Full-service banks are no longer content to wait for wealth to mature and arrive post-IPO. They are traveling back to the point of wealth’s creation, the venture capital ecosystem, to capture the next generation of entrepreneurs and high-net-worth individuals, ensuring their relevance for the next fifty years. This trend represents a fundamental “rebundling” of financial services into fully integrated ecosystems. The strategic rationale, from early client capture to offering differentiated products, is compelling, yet it is set against the immense cultural and operational challenge of integrating the high-risk world of venture capital into the regulated machinery of a global bank. The acquisition of Industry Ventures, a firm with $7 billion in assets and over 1,000 investments, is the prime exhibit. As Goldman Sachs CEO David Solomon stated, the goal is to provide “very, very wealthy clients access to other investment opportunities and products that are hard to access,” a quote that encapsulates the entire strategy.

Anatomy of the Goldman Bet: A Surgical Strike on the Private Market Lifecycle

The Goldman Sachs-Industry Ventures transaction, valued at up to $965 million, is a masterclass in strategic alignment. The structure includes $665 million in upfront cash and equity, supplemented by a significant $300 million in contingent consideration tied to performance through 2030. This long-dated earn-out is a sophisticated integration tool, designed to retain the entire 45-person team by transforming them from employees into long-term partners vested in the merger’s success. It directly mitigates the risk of a talent exodus, a common failure point in such acquisitions.

The target’s profile is equally strategic. Industry Ventures is a 25-year-old specialist in the full venture capital lifecycle, with deep expertise in secondary markets and hybrid funds. As traditional exits like IPOs remain constrained, this secondary market proficiency provides a critical liquidity solution for entrepreneurs and early investors, making it a highly valuable capability. The firm’s historical performance, a net IRR of 18%₁ and a net realized MOIC of 2.2x₁ since its inception, underscores the quality of the platform being acquired.

This was not a cold acquisition. Goldman Sachs Asset Management had been a Limited Partner (LP) in Industry Ventures’ funds for over two decades, and its Petershill Partners unit had held a minority stake since 2019. This long-standing relationship de-risks the deal, suggesting extensive due diligence and ``cultural vetting had occurred long before the final agreement. While the $7 billion in assets under supervision is a notable addition to Goldman’s $540 billion alternatives platform, the true prize is the irreplaceable network and institutional knowledge embedded within the Industry Ventures team. Goldman is buying proprietary deal flow and market intelligence, a talent and network acquisition disguised as an AUM purchase.

The Systemic Shift: An Industry-Wide Scramble for Integrated Ecosystems

Goldman’s move is part of a broader, industry-wide strategic pivot toward creating holistic financial platforms. Competitors are pursuing different layers of the value stack: products, platforms, and plumbing, to achieve the same end goal of ecosystem dominance. Morgan Stanley’s $7 billion acquisition of Eaton Vance, a manager with over $500 billion in AUM, was explicitly designed to add stable, fee-based revenues and scale its wealth management business to oversee $4.4 trillion in client assets. Paired with its $13 billion purchase of E*TRADE, this created a platform spanning the entire wealth spectrum.

JPMorgan, meanwhile, is cornering the market’s “plumbing.” Its acquisition of Aumni, a data analytics platform that has evaluated over $600 billion in invested capital across 17,000 companies, embeds the bank in the core infrastructure of the venture ecosystem. This provides unparalleled data on market trends and deal terms, creating a powerful information advantage. UBS has focused on the next generation of clients, acquiring robo-advisor Wealthfront for $1.4 billion to capture its 470,000 Millennial and Gen Z investors, complementing its internal $200 million UBS Next fintech venture portfolio.

This M&A frenzy is occurring as banks cement their role as the primary financiers of the private markets. As of June 2025, US banks had extended nearly $300 billion in loans to private credit providers and another $285.2 billion to private equity and venture capital funds. This creates a complex dynamic where banks are simultaneously lenders to, competitors of, and now owners of, private market participants, blurring traditional lines and concentrating systemic risk.

The Integration Paradox: Merging Oil and Water

Successfully integrating a venture capital firm into a global bank presents a profound challenge, a true integration paradox.

The Culture Clash

The core operating models are fundamentally opposed. Investment banking is transactional, driven by quarterly performance and short-term deal flow. Venture capital is a patient, long-term business with 5-10 year investment horizons, built on active company-building. This is reflected in their risk appetites: banks are risk-mitigation machines, while VC operates on a “power law” model where a few massive successes offset a majority of failures. The work culture mirrors this divide, pitting the high-pressure, transactional environment of banking against the more strategic, long-term focus of VC.

The LP Alignment Question

Significant conflicts of interest arise. A bank’s wealth management division could become a captive distribution channel for its in-house VC funds, potentially incentivizing advisors to push proprietary products over superior external options. Furthermore, the bank’s position as a lender, M&A advisor, and now equity owner across the ecosystem creates information asymmetries that will attract intense regulatory scrutiny.

The Operational Minefield

VC fund administration is notoriously complex, relying on manual processes for capital calls, distributions, and the subjective valuation of illiquid assets. This clashes with the standardized, automated systems banks require for compliance and efficiency. The underlying data in VC is often unstructured and incomplete, creating a massive technological hurdle for integration into auditable bank reporting systems.1 The success of these mergers will depend on creating a “semi-permeable membrane” model of integration that protects the VC unit’s autonomy while allowing strategic benefits to flow through. Goldman’s decision to place Industry Ventures within its External Investing Group is a tangible attempt at this delicate balance.

Redrawing the Map: Competitive Implications for the Investment Landscape

This trend will accelerate the bifurcation of the private markets. On one side will be the massive, bank-owned platforms offering a bundled suite of services. On the other will be hyper-specialized, independent boutiques that compete on deep domain expertise and agility. The undifferentiated firms in the middle will be squeezed.

For independent VCs, the challenge is to compete against giants that can offer a founder everything from seed funding to an IPO. Their advantage lies in speed, specialization, and a clear alignment of interests, free from the institutional conflicts of a larger bank. For LPs, the “one-stop shop” offers convenience but reduces choice and demands greater diligence regarding conflicts of interest. For entrepreneurs, the proposition is a double-edged sword: access to a bank’s vast resources versus the bureaucracy and potential for slower decision-making that comes with it.

Crucially, the definition of “alpha” for these bank-owned VCs may shift from purely financial returns to a more holistic measure of value. The return on an investment will include not just the fund’s IRR but also the future value of the founder as a wealth management client, the M&A fees generated from the portfolio company, and the market intelligence gained. This creates a competitive dynamic that independent VCs, who live or die by financial returns alone, cannot easily match.

Conclusion: The Great Rebundling and the Future of Financial Services

The acquisition of VC firms by global banks signals “The Great Rebundling.” After decades of specialization, financial institutions are re-integrating to create end-to-end ecosystems that capture and manage wealth across its entire lifecycle. The Goldman bet is a wager that the future of finance will be won not in the public markets, but in the private ecosystems where the next generation of wealth is being forged. Success hinges on solving the integration paradox: fusing the risk-taking culture of venture capital with the scale and discipline of a global bank. The firm that cracks this code will not just lead the market; it will define it.

Goldman Sachs buys venture capital firm Industry Ventures

https://www.reuters.com/legal/transactional/goldman-sachs-buys-venture-capital-firm-industry-ventures-2025-10-13/?utm_

Secular Growth Trends Weather Cyclical Changes - PGIM, accessed October 25, 2025, https://www.pgim.com/investments/article/secular-growth-trends-weather-cyclical-changes

UBS launches UBS Next to further engage with fintechs and the tech ecosystem, accessed October 25, 2025, https://www.ubs.com/global/en/media/display-page-ndp/en-20201027-ubs-next.html