Suppressor Compliance and Trust Services Industry Analysis

Read the original at capraecapitalpartners.substack.com ↗

Thesis: Against

The suppressor compliance and trust services sector is an attractive option for private equity investors, but a risky play for entrepreneurs. Over the past few years, suppressor purchases have seen unprecedented growth. More suppressors were purchased between 2021 and 2024 than the preceding 84 years. Consequently, suppressor compliance services grew in conjunction with the demand surge. This industry momentum is expected to continue, allowing for an opportunity for high returns in the short run. However for those focused on the long-run, such as entrepreneurs and search-fund investors, the underlying risks and lack of recurring revenue sources make it an unattractive option.

Market Overview

Firearm suppressor compliance and trust services is a niche subsector within the firearms market that offers a wide range of solutions for consumers and dealers to comply with NFA requirements when purchasing suppressors. Through several services, businesses aim to assist with creating and handling the numerous legal documents associated with purchasing a suppressor.

TAM

Total Addressable Market (TAM): The U.S. suppressor compliance & trust services sector is a relatively small but rapidly growing niche with an estimated base TAM of $34 million and CAGR of 20%. We estimate the TAM by considering the annual volume of suppressor transactions and the typical “attach rate” and fees for compliance services on each transaction:

● Annual Suppressor Transaction Volume: In recent years, suppressor sales have surged. Historically, only about 1.3 million suppressors were registered in the U.S. by 2017. By May 2021 that figure doubled to 2.66 million, and by January 2024 it reached 3.49 million[1]. Thanks to the new eForms system and reduced wait times, Americans purchased and registered about 2.2 million new silencers between May 2021 and mid-2024, an unprecedented surge[2]. As of July 2024, the total number of civilian-owned suppressors is roughly 4.86 million[3]. This means roughly 2.2 million suppressors were added in just three years (mid-2021 to mid-2024), eclipsing the number added in the NFA’s first 87 years[4].

● For TAM calculations, we use an annualized volume in the hundreds of thousands. While 2024 saw a huge spike (1.4 million silencers registered in the first half of 2024 alone)[5], that was partially a backlog being processed after eForms launch. A more normalized forward run-rate may be on the order of 500,000–800,000 suppressor transfers per year in the near term. This assumes continued strong demand but not every year repeating the extraordinary 2024 spike.

● Attach Rate of Services: Not every suppressor buyer uses an external compliance service, some may file on their own or go through manual processes. However, the attach rate has grown with the rise of streamlined platforms. We assume 50–80% range of suppressor transactions involve a paid compliance service or trust. This includes buyers who set up a paid NFA trust and/or use a facilitation platform. Given the dominance of Silencer Shop and Silencer Central in the market, this rate is likely high. A large majority of suppressor transfers now flow through specialized service platforms or dealers employing them. For instance, Silencer Shop alone has over 1,800 affiliated dealers using its system[6], which likely accounts for a substantial portion of all Class 3 dealers nationwide.

● Fee Stack Assumptions: The revenue per transaction can include multiple service fees. Trust setup fees typically range from $0 to $200. Fingerprinting and document processing fees might add $30–$50. Some dealers or platforms charge a separate filing or convenience fee ($25–$50) for handling the paperwork. In aggregate, an average customer using a full suite of services might generate on the order of $50–$100 in service revenues (excluding tax). For our TAM model, we assume an average of roughly $75 per transaction in revenue to the compliance/trust service providers.

Using these inputs, we can estimate current TAM and see how it varies under different scenarios:

CAGR:

Despite its modest size, this sector has shown explosive growth in line with suppressor adoption. Historically, suppressor registrations have grown between 20–25% CAGR over the past decade. For instance, from 2010 to 2024, the compounded annual growth was over 22%[1]. Even focusing on the last few years, 2017 to 2021 saw a 19% CAGR, and 2021 to 2024 saw a 22% CAGR[2]. This growth accelerated recently as the process hurdles fell. In fact, more suppressors were added between 2021 to 2024 than in the NFA’s first 87 years[3].

Looking ahead, projected growth remains robust but may stabilize to lower double-digits. Industry observers expect suppressor ownership to continue “normalizing” among gun owners. NSSF’s research director noted that what was rare a decade ago “is now a normal occurrence” at ranges and hunting camps[4]. With eForm approvals now often taking days instead of months, the last major barrier to purchase has essentially crumbled. This suggests the suppressor market could sustain strong growth in the near term. If we employ the average CAGR over the different aforementioned periods for the projections, we get a CAGR of 20%.

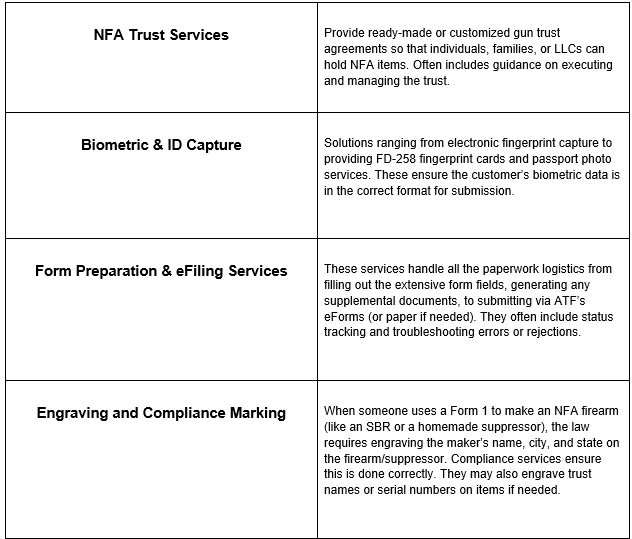

Market Landscape

To better visualize the suppressor compliance & trust services ecosystem, below is a market map of key service categories with examples of providers in each:

Core Growth Drivers

Several key growth drivers are propelling the suppressor compliance/services industry, creating a favorable environment for continued expansion:

● Regulatory Stability and Incremental Reforms: Paradoxically, the NFA regulations, onerous as they are, have been relatively stable over the past few years, giving industry players a stable playing field to optimize against. The major disruptive rule was ATF Rule 41F in 2016, which initially caused a one-time surge since buyers rushed to purchase before the new requirements kicked in[1]. After that adjustment, there have been no new federal restrictions on suppressors, and in fact pro-suppressor lobby groups have successfully relaxed some barriers. For example, the CLEO sign-off was eliminated and replaced by simple notification, which opened up suppressor ownership in jurisdictions where hostile law enforcement had blocked it prior to 2016[2]. Currently 42 states allow suppressor ownership for civilians and for hunting use[3]. This relative regulatory calm, combined with small improvements, has given consumers confidence to buy NFA items without fearing sudden rule changes. Political efforts to deregulate suppressors (Hearing Protection Act, SHUSH Act), while not passed, signal that the climate is, if anything, trending toward more acceptance[4]. Overall, This sutatined stability will facilitate market growth over the next few years.

● Platformization and Ease of Purchase: The emergence of integrated platforms has transformed the industry. By dramatically simplifying the buying process, these platforms have expanded the addressable customer base beyond hardcore enthusiasts to more casual gun owners. Today, a customer can walk into a gun store and complete their suppressor paperwork via a self-service kiosk in minutes[5], or even buy online and complete fingerprints and docs from home. For example, Silencer Central offers financing, mails you a fingerprint kit, submits your eForm, and ships the suppressor to your door once approved, enabling customers to never set foot in a store[6]. These new systems have resulted in higher conversion rates and more repeat purchases as satisfied customers return for additional NFA items. The platform approach also fuels network effects. Silencer Shop’s 1,800+ dealer integrations create broad availability of its service[7], making it the de facto infrastructure for much of the market.

● Dramatic Reduction in Wait Times: Perhaps the most impactful catalyst for the recent surge is the collapse of ATF wait times due to process improvements. The launch of ATF eForms for Form 4 in December 2021, combined with ATF hiring and workflow changes, cut approval times from the 8–12+ month range down to a matter of weeks[8]. As of early 2025, individual Form 4s are often approved in 2–27 days, and trusts in 5–37 days[9]. Moreover, a new process introduced in 2024 runs FBI background checks immediately upon submission, enabling many applications to be approved within hours if there are no red flags[10]. These efficiency gains have directly driven sales and are the key catalyst for the recent surge in suppressor purchases.

● Cultural Normalization and Awareness: The marketing narrative around suppressors has shifted in recent years from exotic, tightly-controlled “silencers” to common safety and convenience accessories and has even been branded as “hearing protection”. Groups like ASA and industry members have educated consumers that suppressors can protect hearing, reduce noise complaints, and improve shooting comfort. Additionally, High-profile gun manufacturers entering the suppressor market have lent legitimacy and visibility to these products[11]. As a result, suppressors are increasingly seen as a mainstream firearm accessory. This normalization drives growth in two ways: more first-time buyers (hunters, sport shooters, etc., who now view a suppressor as a logical next purchase) and existing owners buying multiple suppressors.

● Expansion of Dealer Networks and Kiosk Footprint: On the supply side, more firearms dealers are choosing to become Class 3 SOTs (Special Occupational Taxpayers) to sell NFA items, especially now that handling the paperwork is easier. There were about 5,500 Class 3 dealers in 2016,[12] and this number has likely grown substantially with the suppressor boom. Silencer Shop’s strategy of widely deploying kiosks and onboarding dealers has increased the penetration of NFA sales capability. As of 2023, Silencer Shop had placed kiosks in over 1,800 gun shops across 42 states, meaning a huge portion of gun retailers now has at least the means to sell a suppressor with minimal friction[13]. This has effectively turned suppressor sales from a niche specialty of a few dealers into a widespread offering available at many local gun stores. Furthermore, the convenience of local kiosks reinforces the virtuous cycle of easy buying experience leading to more demand.

Regulatory Barriers and Service Model Implications

Operating in a tightly regulated space, the suppressor services industry is fundamentally shaped by the NFA’s legal requirements. Key regulatory factors, notably ATF Rule 41F, the advent of eForms, and CLEO notification rules, have direct impacts on how services are designed and delivered:

● ATF Rule 41F (2016) : This rule, implemented July 2016, was a key moment for the industry. Prior to 41F, NFA trusts, any trustee could buy an NFA item without submitting fingerprints, photos, or undergoing a personal background check. Trusts also bypassed the need for local law enforcement sign-off. Many buyers formed trusts specifically to exploit these advantages. Rule 41F closed that gap by requiring every “responsible person” of a trust or legal entity to submit fingerprints, a photo, and undergo the background check, and instituted the CLEO notification for all[14]. This had immediate effects on the services model:

○ The demand for NFA trusts initially spiked before 41F’s effective date, as buyers rushed to purchase under the old easier rules[15].

○ After 41F, trusts became somewhat less convenient. As a result, a portion of buyers reverted to filing as individuals. Trust-oriented services had to adapt by emphasizing other trust benefits such as sharing items among family and estate planning rather than speed. Some introduced streamlined trust products. The services model shifted from large one-time comprehensive trusts to more transaction-specific or simplified trusts to keep the process easy under the new rules.

○ Compliance providers also had to build out infrastructure for handling multiple fingerprints and photos for trust clients. For example, if a trust has two trustees, the platform must capture and submit two sets of biometrics. This increased the complexity on the back-end, but companies rose to the challenge by developing software to manage multiple “profiles” per application.

● CLEO Notification (Replacing Sign-off): Before 2016, individual applicants needed sign-off from their Chief Law Enforcement Officer. Rule 41F replaced this with a simple notification requirement in which the applicant (or dealer on their behalf) must send a copy of the Form 4 to the local CLEO, but no approval is needed[16]. This change removed a major barrier to suppressor sales in many areas. For compliance services however, the CLEO notification led to the following effects:

○ Platforms typically automate the CLEO notification, preparing a copy of the form and oftentimes even mailing or emailing it to the appropriate agency for the customer. This became a standard feature of service.

○ The removal of sign-off also meant more individuals now purchase as individuals which likely reduced the proportion of buyers using trusts. Services had to cater equally to individual filers, whereas before 2016 trusts were the dominant mode for many due to the sign-off issue. Now, platforms must seamlessly support both individual and trust filings which, from a software standpoint, means giving users an easy choice and handling two slightly different submission workflows. The Silencer Shop kiosk, for example, has the user choose registration as a Trust, Corporation, or Individual at the final step[17], reflecting how the service model now flexibly accommodates all ownership types.

● ATF eForms System: The introduction of electronic filing (eForms) for Form 4 in late 2021 fundamentally altered service delivery. Previously, even if a company prepared paperwork for a customer, the final submission was via mail, which meant physical fingerprint cards, checks for tax, and paper forms, with the ATF manually entering data on their end. This was slow and labor-intensive. With eForms:

○ Services had to transition to fully digital data handling. Providers that invested early in integrating with eForms reaped rewards. The kiosk infrastructure, which already captured digital fingerprints and stored customer data, became even more valuable as they enabled digital files to be uploaded to ATF instantly[18]. Essentially, eForms supercharged the value proposition of electronic-centric platforms (overnight, a customer’s digital profile became the key to fast submission, whereas old-school dealers who stuck to paper were left with an inferior process).

○ The eForms rollout was not without hiccups – early on there were system slowdowns and learning curves. Compliance service firms often acted as tech support, guiding dealers and customers through account setup, uploading trust documents, etc. Many dealers who were uncomfortable with the new system outsourced the whole filing task to the specialists. In effect, ATF digitizing its end pushed the industry to deepen its tech integration on the front-end.

○ Turnaround times plummeted with eForms, which meant higher throughput for the industry. Previously, a dealer might have been cautious to submit too many applications at once, now, approvals come in daily. Consequently,companies like Silencer Central had to rapidly scale logistics. At one point in 2024 they had 70,000 suppressors in backlog awaiting ATF approval, then suddenly approvals started clearing at record speed, requiring shipping “almost hourly” out of their warehouse[19]. Thus, eForms forced compliance service providers to bolster not just IT but also operational capacity to handle the much faster cycle from sale to delivery. Those that scaled effectively gained a competitive edge.

○ Importantly, eForms also enabled data-driven tracking of submissions and approvals. Many service providers now give customers status updates via online dashboards, and some even crowd-source approval timelines. The digitization has improved transparency, allowing services to manage customer expectations better and reduce support burdens.

.

Risks and Mitigants

Deregulation of Suppressors (Legal Changes Eliminating NFA Status): Proposed bills such as the Hearing Protection Act (HPA) and the SHUSH Act aim to reclassify suppressors as ordinary title I firearms and accessories. If either of these bills pass, the entire compliance process and the services based on it will cease to exist. In other words, the existence of this industry is dependent on the NFA status of suppressors.

● Mitigant: While there is no direct mitigant to this risk, the likelihood of suppressors losing NFA status is relatively low. The Hearing Protection Act had some momentum in 2017 but ultimately failed to pass and subsequent attempts made little progress. Any deregulation in the firearms industry requires strong bipartisan support which can be difficult to obtain.

Political Volatility and Enforcement Climate:Beyond formal deregulation, the industry must always contend with the broader political winds around firearms. A change in administration or ATF leadership could result in stricter enforcement or new rule interpretations that make suppressor transactions more difficult. For example, ATF could institute new requirements like more frequent background checks or limitations on eForms usage. There’s also the threat of individual states imposing bans or onerous regulations on suppressors. And more importantly, negative publicity from crimes involving suppressors can create public relations and legislative risks. If the political climate shifts toward gun control, suppressors could be an easy target given public misconceptions.

● Mitigant: Firms in the industry have always had to face changing regulatory environments and have proven their ability to adapt. From the introduction of rule 41F to the digitization of the compliance process, changes to enforcement had always brought upon new opportunities for profit which firms took advantage of. Therefore, firms are well-positioned to deal with future regulatory changes. In fact, further additions to the compliance process caused by stigma around the dangers of suppressors may even create new services.

Market Saturation or Slowdown in Growth: Another risk is that the explosive growth of the past few years might not be sustainable. Pent-up demand has largely been released in the 2022–2024 surge. It’s possible that many firearms enthusiasts who really wanted a suppressor have now acquired one, and the rate of new adopters could diminish. If annual suppressor sales plateau or only grow at single-digit rates, the service industry’s growth would likewise level off. Additionally, suppressors are durable goods with a long lifespan; unlike consumables, they don’t drive continuous replacement demand. Moreover, a downturn in the economy or declines in overall gun sales could soften suppressor sales, as they’re often a luxury accessory rather than a necessity.

● Mitigants: The current data is yet to show any signs of saturation. And in a country with about 100 million gun owners, only 5 million suppressors are owned. There is ample room for growth if even a fraction of those owners decide to try a suppressor. As awareness campaigns continue and more ranges allow/encourage suppressed shooting, the pool of potential customers is expanding.

Looking at all these risks together, it is evident that the industry’s strong momentum is highly vulnerable. While there are mitigants for each of these risks, they will likely do little to offset the implications. If suppressors are reclassified through deregulation, or if they are banned by states in an attempt for stronger regulation, the industry will cease to exist. Therefore, the industry is always at a high risk of irrelevance. Regulation aside, the strong growth the industry is currently seeing can be diminished by a wide range of factors given the nature of the suppressors themselves. These risks, however, should not overshadow the short-term potential the industry has due to strong demand. Suppressor compliance services may not be a safe long-term investment, but have the potential to be a rewarding short-term play.

Investment Considerations (Recurring Revenue, Scalability, and Consolidation)

From a private equity or venture capital lens, the suppressor compliance & trust services sector presents a unique blend of subscription-like revenue patterns, high infrastructure leverage, and a fragmented competitive landscape ripe for consolidation. Key considerations include:

● Recurring Revenue and Customer Lifetime Value: Although on the surface the business might seem transactional with(each suppressor purchase generating a one-time fee, in practice the model has some elements of recurring revenue and strong customer retention:

○ “Trust Ecosystems” and Customer Retention: Once a customer establishes an NFA trust or profile with a service, they are likely to use that same service for subsequent NFA transactions. The initial transaction effectively onboards the customer into an ecosystem where their documents are stored, their fingerprints are on file, and they are familiar with the process. This leads to repeat purchases flowing through the same platform with minimal additional cost of acquisition. Thus, while the revenue per customer per year might vary, over a multi-year period an active NFA consumer provides a stream of fees or margin contributions.

○ Form 1 Repeatability: The same customer who buys a commercial suppressor (Form 4) might later decide to make their own NFA firearm via Form 1, such as converting an AR-15 pistol into a short-barreled rifle or even constructing a suppressor from a kit (where legal). The compliance service firms can capture this by offering Form 1 filing assistance and. For instance, after simplifying Form 4s, Silencer Shop and others began providing Form 1 generators and engraving solutions[20]. Every Form 1 filed is another revenue event, and enthusiasts may do several. This adds to recurring usage beyond just store-bought suppressors.

○ Ancillary Recurring Services: Some companies are exploring maintenance plans or memberships. If a significant installed base of suppressors exists, services like periodic cleaning, repairs, or upgrades could become subscription-like offerings. While nascent, these ideas indicate the potential to smooth revenue between spikes of form filings.

○ Firearm Dealer SaaS: Some businesses in the industry offer SaaS platforms to dealers that encompass all the services required for compliance. From trust creation to fingerprint uploads, these platforms enable dealers to efficiently run through the compliance process. With there being thousands of dealers across the country, dealer SaaS contains a large target market, making it a profitable recurring revenue source.

○ It’s also worth noting the geographic expansion acts somewhat like recurring revenue in aggregate. As new states legalize suppressor purchases the industry gets a bump of new customers who then repeat. For entrepreneurs, the takeaway is that the business isn’t purely one-and-done transactional. There is a sticky customer relationship and multiple monetization opportunities over time from each user acquired, which can justify higher customer acquisition cost and investment in onboarding technology.

● Scalability and Infrastructure Leverage: The leading companies have already invested heavily in infrastructure, both physical kiosks and digital platforms, creating a scalable foundation that yields high incremental margins as volume grows:

○ Kiosk & Dealer Network Scale: Silencer Shop’s1,800 kiosks are a significant capital deployment that would be very difficult for a new entrant to replicate quickly[21]. Now that they are in place across 42 states, adding more customers or transactions does not require linear cost increases and each kiosk can handle many applications per day. The penetration of Silencer Shop’s network is estimated to cover a substantial portion of all active NFA dealers. This creates a quasi-barrier to entry as any competitor trying to deploy a similar network from scratch would face high upfront costs and would be chasing an incumbent with established relationships.

○ Digital Infrastructure and Automation: A core part of these businesses is software for managing customer databases, form generators, eForms integration, etc. These systems have high initial development cost but then very low marginal cost per additional application processed. As volumes exploded from 100k to 700k+ per year, the companies that had automated processes simply ramped up throughput with minor tweaks. For example, Silencer Central, upon seeing wait times drop, was able to ramp shipments to 2,000 orders/hour with an automated distribution system[22], reflecting foresight in scaling operations. The ATF’s improved processing actually lowers the working capital burden on companies, allowing them to handle more sales without proportional capital tie-up. In effect, the operating leverage is significant with fixed costs spread over an ever-growing number of transactions. This should improve profit margins as the surge of 2022–2024 is digested, provided they have the right-size staffing post-backlog. For investors, the scalable nature of these platforms suggests the potential for high EBITDA margins at scale, especially for the market leaders.

● Fragmentation and Consolidation Opportunities: The current market structure is a mix of a few dominant platforms and many small players, which is often attractive for consolidation plays:

○ Market Leaders vs. Fragmented Tail: Silencer Shop and Silencer Central stand out as the two largest participants, but beyond them lies a long tail of small businesses consisting of independent NFA gun trusts providers, niche software tools, and hundreds of individual Class 3 dealers who do their own paperwork without an outside platform. Even among dealers, some large-volume NFA dealers like Capitol Armory or Kennesaw Silencer operate independently with their own customer bases. This suggests the industry is moderately fragmented, especially on the service fee capture side. Silencer Shop’s model is more B2B2C (serving dealers), and Silencer Central is B2C (direct dealer).

○ White Space and M&A Possibilities: One area for potential consolidation is merging compliance tech with distribution. Silencer Shop is strong in both, essentially acting as a distributor and tech provider. An independent dealer network or a major wholesaler could find value in acquiring a tech platform to remain competitive. Conversely, a tech-oriented service might merge with a suppressor manufacturer or distributor to secure supply and improve margins.

○ For founders, these factors suggest an opportunity to build a platform. By injecting capital and consolidating a few pieces, one could accelerate growth and achieve a commanding position before the window closes. The Inc. 5000 rankings show Silencer Central with 165% three-year growth (2019–2022)[23], indicating high growth but perhaps slowing as it scales. There may be a window for founders to take chips off the table or partner with investors for the next expansion phase. An investor could help professionalize operations, integrate vertically and drive margin expansion through tech and scale. The exit opportunities could include strategic sales to larger firearm industry players or to broader outdoor/gun industry roll-ups.

Search funds Beware:

Suppressor compliance services have seen immense growth over the past few years, and we project a 20% CAGR in the near future. However, for searchers looking for a low risk high reward investment, it’s best to steer clear of this industry. There is little evidence to support the expectation that current growth levels will be sustained over a long period of time. Moreover, Suppressor compliance services are solely dependent on the status of suppressors under the NFA which can be subject to change. This creates a risk which is relatively difficult to mitigate. On top of this, the industry is already dominated by two key players, Silencer Shop and Silencer Central. These two firms already have established relationships with dealers across the nation and offer services catering to all steps of the compliance process. Investing in a suppressor compliance firm may reap benefits in the short-term due to the growth trend, but is bound to face headwinds over the long run due to the underlying risks and competition.

Research Credit: Ibraj Alam

Managing Editor: Nate Park, Jeremy Bratanata

[1]https://www.thefirearmblog.com/blog/silencer-saturday-369-atf-silencer-industry-data-44819362#:~:text=The%20dip%20in%20applications%20from,What%20is

[2]https://www.thefirearmblog.com/blog/silencer-saturday-369-atf-silencer-industry-data-44819362#:~:text=The%20dip%20in%20applications%20from,What%20is

[3]https://www.guns.com/news/2024/10/09/suppressor-numbers-nearly-double-in-3-years-now-486-million-and-counting#:~:text=Suppressor%20Numbers%20Nearly%20Double%20in,22%20of%20those%20allowed

[4]https://smokinggun.org/new-data-shows-troubling-surge-in-silencer-sales/#:~:text=As%20discussed%20here%2C%20groups%20like,some%20form%20of%20hearing%20protection

[5]https://www.silencershop.com/blog/silencer-shop-kiosk#:~:text=Your%20visit%20to%20the%20Silencer,as%20little%20as%20five%20minutes

[6]https://smokinggun.org/new-data-shows-troubling-surge-in-silencer-sales/#:~:text=Silencer%20retailers%20have%20also%20worked,collect%20personal%20information%20and%20fingerprints

[7]https://www.silencershop.com/blog/silencer-shop-kiosk#:~:text=Silencer%20Shop%20Kiosks%20are%20located,completed%20in%20just%20five%20minutes

[8]https://www.thefirearmblog.com/blog/silencer-saturday-369-atf-silencer-industry-data-44819362#:~:text=Waiting%20long%20stretches%20of%20time,from%202017%20to%202021%20are

[9]https://www.thefirearmblog.com/blog/silencer-saturday-369-atf-silencer-industry-data-44819362#:~:text=Waiting%20long%20stretches%20of%20time,from%202017%20to%202021%20are

[10]https://siouxfalls.business/meteoric-growth-leads-to-expansion-plans-at-silencer-central/#:~:text=application%20for%20a%20silencer

[11]https://smokinggun.org/new-data-shows-troubling-surge-in-silencer-sales/#:~:text=Finally%2C%20more%20companies%20are%20producing,with%20threaded%20barrels%20to%20accept

[12]https://rocketffl.com/ffl-license-application-sot-and-inspection-statistics/#:~:text=FFLs%20%20and%C2%A0becoming%20an%20SOT

[13]https://www.silencershop.com/blog/silencer-shop-kiosk#:~:text=You%20can%20find%20a%20kiosk,specifically%20for%20dealers%20with%20kiosks

[14]https://www.thefirearmblog.com/blog/silencer-saturday-369-atf-silencer-industry-data-44819362#:~:text=The%20dip%20in%20applications%20from,What%20is

[15]https://www.thefirearmblog.com/blog/silencer-saturday-369-atf-silencer-industry-data-44819362#:~:text=The%20dip%20in%20applications%20from,What%20is

[16]https://smokinggun.org/new-data-shows-troubling-surge-in-silencer-sales/#:~:text=owned%20by%20the%20U,7%20million%20silencers%20between%201934

[17]https://www.silencershop.com/blog/silencer-shop-kiosk#:~:text=the%20keyboard%202,method%3A%20Trust%2C%20Corporation%2C%20or%20Individual

[18]https://www.silencershop.com/blog/silencer-shop-kiosk#:~:text=the%20ATF%20when%20your%20eForm,4%20is%20submitted

[19]https://siouxfalls.business/meteoric-growth-leads-to-expansion-plans-at-silencer-central/#:~:text=Here%E2%80%99s%20another%20powerful%20data%20point%3A,customer%E2%80%99s%20application%20for%20a%20silencer

[20]https://www.nationalguntrusts.com/blogs/nfa-gun-trust-atf-information-database-blog/atf-releases-2024-fact-sheet-facts-and-figures-for-fiscal-year-2024?srsltid=AfmBOooO-VPfD7hoEg4KgtNVq1wX_CSD9oAb1E9FSkNsqmggZLOtL9yL#:~:text=,ATF%20Form%20Generators

[21]https://www.silencershop.com/blog/silencer-shop-kiosk#:~:text=You%20can%20find%20a%20kiosk,specifically%20for%20dealers%20with%20kiosks

[22]https://siouxfalls.business/meteoric-growth-leads-to-expansion-plans-at-silencer-central/#:~:text=Vertical%20construction%20will%20get%20underway,be%20converted%20into%20office%20space

[23]https://www.inc.com/profile/silencer-central#:~:text=Silencer%20Central%20is%20a%202025,Stage%3A%20Enduring%20Impact%2C%20Company

[1]https://congressionalsportsmen.org/news/recent-suppressor-registrations-eclipse-numbers-for-the-nfas-first-eight-decades-combined/#:~:text=In%20a%20recent%20Freedom%20of,of%20the%20middle%20of%202024

[2]https://congressionalsportsmen.org/news/recent-suppressor-registrations-eclipse-numbers-for-the-nfas-first-eight-decades-combined/#:~:text=In%20a%20recent%20Freedom%20of,of%20the%20middle%20of%202024

[3]https://congressionalsportsmen.org/news/recent-suppressor-registrations-eclipse-numbers-for-the-nfas-first-eight-decades-combined/#:~:text=and%20hunters%20are%20buying%20suppressors,pursuits%20safer%20and%20more%20enjoyable

[4]https://smokinggun.org/nssf-americans-bought-1-4-million-silencers-in-first-six-months-of-2024/#:~:text=More%20recently%2C%20when%20the%20NSSF%E2%80%99s,%E2%80%9D

[1]https://smokinggun.org/new-data-shows-troubling-surge-in-silencer-sales/#:~:text=Update%202021%2C%E2%80%9D%2016%2C%20https%3A%2F%2Fwww.atf.gov%2Ffirearms%2Fdocs%2Freport%2F2021,percent%20increase%20is

[2]https://congressionalsportsmen.org/news/recent-suppressor-registrations-eclipse-numbers-for-the-nfas-first-eight-decades-combined/#:~:text=In%20a%20recent%20Freedom%20of,of%20the%20middle%20of%202024

[3]https://congressionalsportsmen.org/news/recent-suppressor-registrations-eclipse-numbers-for-the-nfas-first-eight-decades-combined/#:~:text=In%20a%20recent%20Freedom%20of,of%20the%20middle%20of%202024

[4]https://congressionalsportsmen.org/news/recent-suppressor-registrations-eclipse-numbers-for-the-nfas-first-eight-decades-combined/#:~:text=and%20hunters%20are%20buying%20suppressors,pursuits%20safer%20and%20more%20enjoyable

[5]https://smokinggun.org/nssf-americans-bought-1-4-million-silencers-in-first-six-months-of-2024/#:~:text=reporting%20%2C%20this%20updated%20total,4%20million%20silencers

[6]https://www.silencershop.com/blog/silencer-shop-kiosk#:~:text=Silencer%20Shop%20Kiosks%20are%20located,completed%20in%20just%20five%20minutes