Range Safety & Air Filtration Systems Industry Analysis

Read the original at capraecapitalpartners.substack.com ↗

Investment Thesis

The U.S. range safety & air-filtration sector is a $3–5B compliance-driven market anchored in the ~6,000 commercial and law-enforcement indoor ranges nationwide. The industry is highly fragmented, with hundreds of small HVAC contractors, environmental engineers, and niche range specialists controlling local markets but no scaled national provider. Core offerings include specialized HVAC/HEPA systems, filter replacements, compliance testing, and OSHA/EPA audits creating sticky, recurring revenue streams that resemble steady cash flow.

Growth is supported by 8–10% projected CAGR, driven by enforcement of rules around airborne lead exposure alongside modernization of law enforcement and military training ranges backed by state and federal budgets. Rising recreational shooting participation and consumer health awareness pose as main growth drivers giving rise to attractive investment dynamics in terms of low acquisition multiples and strong opportunity to bundle adjacent compliance services.

Overall, the sector presents a defensible, recurring-revenue niche with resilient demand, clear compliance tailwinds, and significant white space for a scaled consolidator to capture share and expand margins.

Industry Overview

The U.S. Range Safety & Air Filtration industry is a fragmented environmental control and compliance sector serving approximately 6,000 commercial and law-enforcement indoor shooting ranges nationwide[1]. Core offerings include specialized HVAC and HEPA air-exchange systems, negative-pressure room designs, high-efficiency filters, and periodic OSHA/EPA-compliant testing. These systems typically include dedicated supply and exhaust air systems, negative-pressure configurations, laminar airflow, and HEPA-level filtration to protect both shooters and range personnel from elevated lead exposure risks[2].

As of 2025, the global indoor shooting range ventilation market size has reached $814.7M indicating the ever growing emphasis on safety and regulatory compliance in indoor firearms facilities. It is characterized and dominated by local HVAC integrators and specialized firms with limited geographic scope and no dominant national player. Many operators are small, founder-run firms with limited geographic reach, creating opportunities for consolidation. The market is experiencing vigorous expansion with a projected CAGR of 6.2% from 2025 to 2033[3]. This growth primarily stems from stricter enforcement of OSHA and EPA standards on airborne lead exposure, increasing investments in law enforcement and military infrastructure especially with the growing geopolitical tensions in the United States, alongside rising participation in recreational shooting sports[4] and heightened awareness of indoor air quality standards.

Overall, the industry is compliance driven, with recurring revenue anchored in consumables: filters, testing contracts and certification audits every few months[5]. This creates a perfect incubator for a recurring-revenue niche with resilience to economic cycles and strong parallels to other regulated environmental services industries.

Market Size & Growth

Total Addressable Market - $3-5B (U.S only)

The U.S market for indoor range ventilation and air-filtration systems is estimated at $3–5B annually. This figure was built from the bottom up with an approximate of 6,000 commercial and law-enforcement indoor shooting ranges nationwide, with an average per shooting range spend ranging anywhere from $500K- $833K. This figure includes initial HVAC/HEPA installations, retrofit projects & compliance services. Key drivers that underpin the Total Addressable Market are regulatory requirements in terms of OSHA and EPA standards, HEPA exhaust, lead exposure lawsuits and public health studies[6] and modernization of facilities by commercial operators and agencies.

Serviceable Available Market - $2.1B

The serviceable Available Market (SAM) addresses the portion of the TAM made up of shooting ranges that actively invest in professional grade ventilation upgrades and filtration systems. With this model, we approximate 75% based on CDC/NIOSH data that actively do. Applying this proportion to the total market (~6,000), it yields a SAM of roughly $2.1B. This sector is characterized by ranges that are subject to stricter oversight with law enforcement, urban commercial facilities that are proactively mitigating legal exposure.

Serviceable Obtainable Market - $200M

The serviceable Obtainable Market (SOM) represents the realistic share of a scaled consolidator/platform that a company could reasonably capture, given the industry’s fragmentation and competitive landscape. Assumptions are around the fact that no national player exists even if leaders hold low- single digit share and that a scaled platform could target 5-10% market share through acquisitions, DSO contracts and other distributor partnerships. This equates to approximately $150-300M and so, the SOM represents the revenue ceiling for a scaled PE-backed platform after consolidation and standardization, mirroring roll-up dynamics seen in regulated environmental services.

CAGR

To build a projected CAGR from the bottom up using these assumptions and statistics; the number of indoor shooting ranges in the U.S. has remained relatively stable, with commercial openings offset by closures, resulting in a baseline facility growth rate of ~0–1% annually. In terms of compliance adoption growth, only ~65–70% of ranges consistently follow OSHA/EPA ventilation and lead-dust standards today. With stricter federal oversight and state-level enforcement post-2020, adoption is climbing, bringing in a reasonable assumption that there’s been +3–4% CAGR in compliance penetration until saturation (~90%). Recurring consumables such as HEPA filters, air-quality tests, and OSHA audits rise with product price inflation of about 2–3% per year. This contributes an additional +4–5% CAGR on per-facility spend.

Taking into account all these growth factors, and multiplying them, this gives a combined CAGR of about ~8–10%. This figure represents the potential growth that will come from tightening environmental regulations, rising modernization budgets for law-enforcement ranges, and expanded adoption of compliance-driven recurring services.

Market Segmentation

The shooting ranges market shows good promise in terms of fragmentation. It is typically segmented by Type, Application and Region.

By Type:

● Indoor Shooting Ranges:

Indoor shooting ranges represent a major part of the addressable market[7] for advanced HVAC and HEPA air-exchange systems. Such facilities require innovative ventilation to maintain negative air pressure, consistent laminar airflow, and HEPA level exhaust filtration to prevent lead dust migration into occupied areas. With about 16,000-18,000 indoor ranges nationwide comprising commercial, law-enforcement and military of which ~6000 make up commercial facilities that require indoor ventilation systems constituting the bulk of the TAM. These ranges also generate recurring revenue opportunities via filter replacement, air-quality testing and compliance audits every 6-12 months[8].

● Outdoor Shooting Ranges:

Outdoor facilities require minimal specialized ventilation because natural airflow disperses airborne particulates[9]. While some operators may invest in localized filtration for covered firing lines or adjacent indoor classrooms, the revenue contribution from outdoor ranges is marginal relative to indoor facilities. As a result, the outdoor segment represents Application:

● Law Enforcement & Government Agencies

Law enforcement ranges account for the largest share of spend (~50–55%) in the U.S. indoor range ventilation market. From police departments to federal facilities that operate high-volume indoor ranges subject to strict OSHA/EPA oversight. Given the possibility of lead exposure, these agencies invest in fixed, high capacity HVAC/HEPA systems with long-term service contracts. Since budgets are tied to federal funding cycles, demand is often less price-sensitive and more compliance-driven. Recurring revenue stems from mandated air-quality audits, filter replacements, and system recalibration every 6-12 months.

● Commercial & Recreational Operators

Commercial ranges represent ~35–40% of the market and are typically membership-driven or pay-per-use facilities in urban and suburban areas. Although not compliance-driven, operators view ventilation systems as brand differentiators and legal safeguards, Many older ranges undergoing retrofits, creating a large mid-market opportunity. This segment is highly fragmented, composed of thousands of independent operators, making it especially attractive for consolidation and service bundling[10].

● Military Training Facilities

Military and National Guard facilities make up a smaller but high-value segment (~10–15%). These sites demand large-scale, high-throughput systems capable of handling sustained ammunition use. Procurement is complex, but once secured, these projects generate significant ongoing service commitments. Military ranges also set the technical standard for air-quality requirements, influencing commercial and law enforcement adoption.

Roll up Strategy

The range safety & air-filtration industry is an extremely fragmented, compliance-driven niche, with hundreds of regional HVAC contractors, environmental engineering firms, and niche range-specialist integrators serving ~6,000 commercial and law-enforcement facilities across the U.S. No single operator currently controls more than a low-to-mid single-digit share, creating a strong foundation for a regional and national consolidation strategy[11].

Most local HVAC and engineering vendors operate with limited scale, manual processes, and local customer relationships[12]. Many are founder or family-run businesses, often without clear succession plans. Valuations remain attractive, with most trading at 3–5× EBITDA, reflecting modest margins. A private equity-backed platform could acquire such operators at low multiples and achieve 2–3× multiple arbitrage upon scaling, mirroring other compliance-driven environmental service roll-ups[13].

By aggregating regional players into a unified platform, a consolidator could unlock significant value through centralizing customer service, logistics, compliance reporting and bulk procurement to negotiate lower supplier pricing and expand gross margins. Introducing uniform processes for audits can improve consistency and scalability for law enforcement and large commercial accounts. A major differentiator could also boil down to tech-enabled compliance tracking, including cloud-based dashboards to log airflow metrics and HEPA filter changes.

Such systems would reduce both administrative burden for operators and increase vendor stickiness, commanding 8-10x EBITDA exit multiples[14]. Beyond ventilation and filtration, a scaled consolidator could bundle compliance- driven services such as ammunition component recycling, ballistic containment systems, occupational safety audits, etc.

Headwinds

The range safety & air-filtration industry faces several structural and operational challenges that can slow consolidation and adoption. It carries a highly fragmented vendor landscape[15] since the sector is dominated by small HVAC contractors, environmental engineers, and niche-range service providers, each operating regionally with limited scale creating challenges for consolidation and operational processes across the industry. Niche Compliance-driven sectors are usually characterized with high upfront spend per facility, which can be a significant barrier for commercial ranges operating on thin margins.

While OSHA/ EPA help provide national standards[16], state and local enforcement can be inconsistent. Some jurisdictions actively inspect and penalize non-compliance and others lack determined oversight. This can slow down adoption in commercial segments, particularly among smaller independent ranges. Such recreational ranges often operate on slim unit economics. Owners view ventilation upgrades and compliance testing as a cost center, leading to reluctance, inconsistency and ultimate pushback against upselling.

Furthermore, military facilities represent high-value opportunities, but their procurement cycles are lengthy and bureaucratic[17]. Federal contracting requires certifications, bidding processes and political alignment, all of which can deter and discourage smaller consolidators from entering this segment without significant resources. Despite the well-documented risks of lead exposure, many commercial operators and even some law enforcement facilities continue to rely on outdated systems or insufficient testing protocols. This low awareness, especially outside high-scrutiny urban markets, reduces the urgency for proactive investment[18].

Tailwinds

Despite structural challenges, the range safety & air-filtration industry benefits from strong regulatory, operational, and market tailwinds that create durable growth opportunities. Considering the post-2020 scenario, federal and state-level inspections have become more frequent[19], with penalties and lawsuits raising compliance urgency. This regulatory tightening calls for a discretionary, non-negotiable compliance requirement. Audits are required to happen every 6-12 months, this recurring cycle creates sticky, subscription-like revenue streams for vendors and ensures demand resiliency even in downturns.

State and federal funding initiatives are fueling upgrades of aging police and training ranges. These contracts often entail multi-year service agreements that lock in recurring consumables and compliance testing revenue, anchoring the industry’s demand base. Furthermore, public health studies[20] have highlighted the dangers of chronic lead exposure for range staff and frequent shooters. Risk of high-profile lawsuits and insurance pressures force operators to prioritize compliance.

With no dominant national provider and hundreds of small, founder-run firms, the sector is structurally positioned for consolidation. A scaled platform could leverage back-office efficiencies, procurement synergies, and tech-enabled compliance services to capture multiple arbitrage[21].

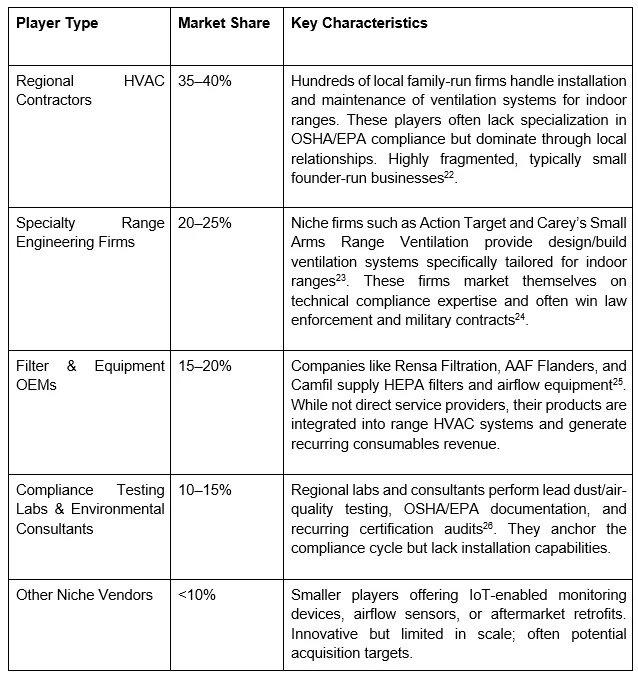

Competitor Landscape

Barriers to Entry

The range safety & air-filtration industry presents moderate-to-high barriers to entry, primarily due to technical, regulatory, and trust-based requirements. OSHA/EPA and NIOSH standards have strict stipulations on airborne lead exposure, airflow velocity (≥50 ft/min) and negative pressure design[1]. Designing compliant ventilation systems requires specialized engineering knowledge. Indoor range projects often require local building permits, environmental approvals, and compliance sign-off[2]. Failures expose vendors to liability risk if staff or patrons are harmed by lead exposure. This legal sensitivity pushes operators toward established firms with proven track records. Furthermore, developing full-service capabilities requires upfront investment in specialized equipment and lab testing capabilities. Military and law enforcement procurement contracts also involve lengthy certification processes that deter undercapitalized entrants[3]. Indoor range projects often require local building permits, environmental approvals, and compliance sign-off. Failures expose vendors to liability risk if staff or patrons are harmed by lead exposure.

Once a facility installs a ventilation system, it is typically locked into the same vendor for ongoing filter replacement, testing, and service contracts. Switching vendors requires administrative effort, staff retraining, and potential compliance disruption, creating friction even when lower-cost alternatives exist. Filter and equipment manufacturers often sell through established HVAC distributors[4]. New entrants face challenges accessing procurement channels or negotiating favorable pricing without scale.

Summary

The U.S. range safety & air-filtration industry is a fragmented, compliance-driven environmental services niche with a total addressable market of $3–5B across ~6,000 commercial and law-enforcement indoor shooting ranges. The market is characterized by technical complexity, regulatory enforcement, and recurring compliance cycles that drive resilience even in downturns.

Growth is projected at 8–10% CAGR, fueled by tightening OSHA/EPA standards, modernization budgets for law enforcement, and recurring demand for filter replacement and testing. The vendor base is dominated by regional HVAC firms, specialty range engineering providers, and consumables OEMs: none of which control more than low-single-digit share. Barriers to entry include high capital intensity, regulatory credibility, and sticky vendor relationships, which protect incumbents but also make acquisition-led growth the most efficient path to scale. Tailwinds such as federal funding, heightened liability awareness, and technology-enabled compliance further reinforce long-term defensibility.

For investors, the opportunity is rooted in the sector’s structural fragmentation, recurring compliance requirements, and regulatory tailwinds. Regional operators can be consolidated into a scaled platform, where operational efficiencies, bulk procurement, and standardized compliance protocols drive meaningful margin expansion. Over time, layering in adjacent compliance services and technology-enabled monitoring tools can further increase customer stickiness and valuation resilience, positioning the sector as an attractive long-term consolidation play within regulated environmental services.

Research Credit: Twisha Puranik Managing Editor: Nate Park, Jeremy Bratanata

[1] https://www.osha.gov/sites/default/files/publications/OSHA3772.pdf

[2] https://archive.cdc.gov/www_cdc_gov/niosh/topics/ranges/default.html?

[3] https://sageuw.com/wp-content/uploads/Lead-Management-OSHA-Compliance-for-Indoor-Ranges.pdf

[4] https://www.rensafiltration.com/industries/shootingranges

[1] https://www.cdc.gov/mmwr/preview/mmwrhtml/mm6316a3.htm?

[2] https://growthmarketreports.com/report/indoor-shooting-range-ventilation-market

[3] https://growthmarketreports.com/report/indoor-shooting-range-ventilation-market

[4] https://www.grandviewresearch.com/industry-analysis/shooting-ranges-market-report

[5] https://www.actiontarget.com/at-short-article/ventilation-matters-advanced-hvac-for-any-shooting-range

[6] https://www.cdc.gov/mmwr/preview/mmwrhtml/mm6316a3.htm

[7] https://www.grandviewresearch.com/industry-analysis/shooting-ranges-market-report

[8] https://www.epa.gov/rmp/how-often-must-compliance-audits-be-performed

[9]https://www.giiresearch.com/report/grvi1575249-shooting-ranges-market-size-share-trends-analysis.html?

[10]https://www.giiresearch.com/report/grvi1575249-shooting-ranges-market-size-share-trends-analysis.html?

[11] https://telescope.ac/latest-market-news/shooting-ranges-market

[12] https://glbainc.com/2025-business-valuation-trends-for-hvac-plumbing/

[13] https://www.raw-selection.com/market-reports/hvac-services-market-report/

[14]https://www.neumetric.com/integrating-compliance-and-risk-management/

[15] https://cfma.org/articles/state-of-play-why-the-hvacr-market-is-ripe-for-consolidation

[16] https://www.osha.gov/sites/default/files/publications/OSHA3772.pdf

[17] https://sageuw.com/wp-content/uploads/Lead-Management-OSHA-Compliance-for-Indoor-Ranges.pdf

[18] https://archive.cdc.gov/www_cdc_gov/niosh/topics/ranges/default.html

[19] https://www.nssf.org/event/osha-compliance-for-shooting-ranges-preparing-for-inspections/

[20] https://ehjournal.biomedcentral.com/articles/10.1186/s12940-017-0246-0

[21] https://www.health.ny.gov/environmental/lead/target_shooting/docs/control_lead_at_shooting_range.pdf